Artikelen

Trading journal-velden die echt worden gereviewd

De velden die een echte tradingweek overleven, en de velden waardoor journals na vijftien sessies stilvallen.

5 min leestijdTradeways#Tradingjournaal#Playbook

De meeste journals mislukken omdat de velden vastleggen wat makkelijk te typen is, niet wat nuttig is om te reviewen. Een rij die vraagt om een moodscore van 1 tot 10 en een vrije tekstparagraaf wordt twee weken ingevuld en stopt daarna stilletjes. Journals die blijven werken, zijn de journals waarin execution data automatisch wordt vastgelegd, intent in een zin past en reflectie uit twee checkboxes bestaat. Al het andere is frictie die concurreert met de volgende trade.

De velden die ertoe doen

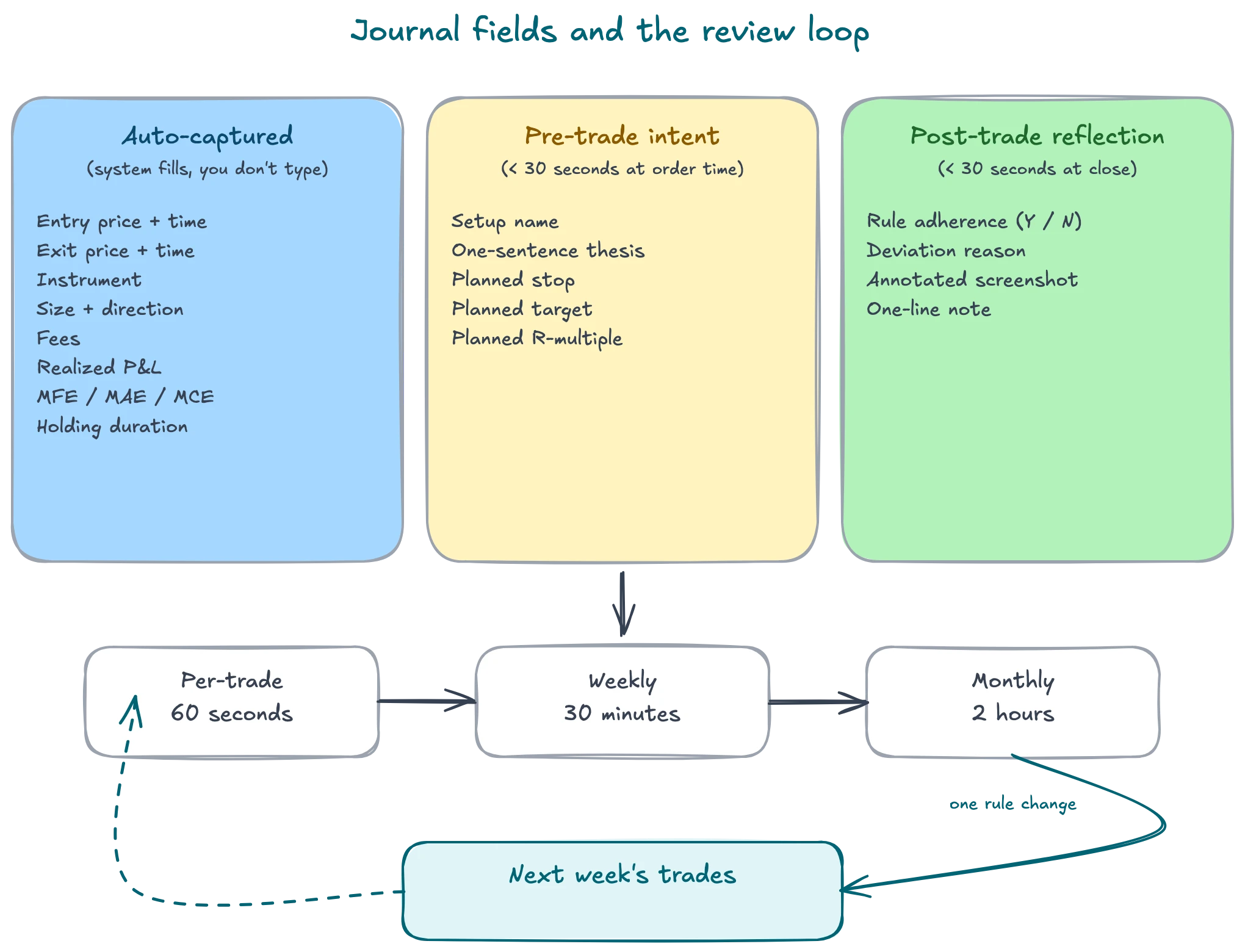

Een journal verdient zijn plek met ongeveer twaalf velden, niet meer. Groepeer ze op basis van wie ze invult: het systeem, jij voor de trade, jij na de trade.

Automatisch vastgelegde execution data. Deze komen uit de fill-data van de broker en de price feed. Je typt ze nooit zelf.

- Entryprijs en timestamp

- Exitprijs en timestamp

- Instrument en contractmaand

- Positiegrootte en richting

- Kosten en commissies

- Gerealiseerde P&L (in geld en in ticks)

- MFE, MAE, MCE (in geld)

- Holding duration

Pre-trade intent. Ingevuld op het moment dat de order live gaat, in minder dan dertig seconden. Als het langer duurt, sla je het over wanneer de tape snel beweegt.

- Setupnaam uit je playbook

- Thesis in een zin (waarom dit, waarom nu)

- Geplande stop en gepland target (prijslevels)

- Geplande R-multiple

Post-trade reflectie. Ingevuld bij het sluiten, ook in minder dan dertig seconden. Twee checkboxes en een regel.

- Regel gevolgd: ja of nee

- Reden voor afwijking (alleen bij nee): een keuze uit een vaste lijst (achtervolgd, stop verplaatst, size verhoogd, fat-finger, nieuws genegeerd)

- Geannoteerde screenshot

- Eenregelige notitie (wat zou je anders doen)

Twaalf tot vijftien velden per trade. Alles daarboven is decoratie.

Wat je weglaat

Moodscores van 1 tot 10 overleven geen ochtend met vijf trades. Bij de derde entry van de dag ben je er al niet meer eerlijk over, en de kolom wordt ruis die elke correlatie vervuilt die je later probeert te draaien. Als emotie ertoe doet, leg die dan vast als een binaire regelafwijking ("buiten plan getraded omdat ik tilted was") in plaats van als een getal.

Generieke tags zoals "goede trade" en "slechte trade" vertellen je wat je al uit de P&L-kolom weet. Ze vormen een vocabulaire dat de echte oorzaak verbergt, en die oorzaak zit in de reden voor afwijking of in de setupnaam.

Essays van meerdere paragrafen per trade zijn een ander faalpatroon. Ze voelen productief, kosten vijftien minuten en je stopt na twee weken. De eenregelige notitie is genoeg. Als een trade echt meer context nodig heeft, hoort die in de wekelijkse review als case study, niet in de rij.

Het principe is simpel. Elk veld moet automatisch worden ingevuld of minder dan tien seconden kosten. Velden die een paragraaf nodig hebben, horen in de review, niet in de rij.

De drie reviewritmes

Een journal is een schrijf-/leessysteem. De meeste traders bouwen alleen de schrijfkant. De leeskant is waar regelwijzigingen ontstaan, en die draait op drie ritmes.

Per trade, 60 seconden. Direct na de close, terwijl de chart nog op het scherm staat. Twee klikken: regel gevolgd ja of nee, reden voor afwijking als het nee is. Een zin. De screenshot wordt automatisch door het platform vastgelegd of geplakt. Dat is de hele entry. Alles wat op dit moment langer duurt, houd je geen maand vol.

Wekelijks, 30 minuten. Vrijdag na sluiting of zondagavond. Sorteer de trades van de week op setupnaam. Bekijk per setup de gerealiseerde P&L naast MFE en bereken de ratio realized / MFE voor de groep (zie Maximum Favorable Excursion voor waarom deze ratio de schoonste meting is van exitkwaliteit). Markeer een ding om volgende week te veranderen. Een ding, geen vijf. Zet het bovenaan het plan voor volgende week.

Maandelijks, 2 uur. Volledige dataset, alle gesloten trades. Bereken hit rate, gemiddelde R en mediane realized / MFE per setup. Sorteer setups op expectancy. Schrap de slechtste setup volledig voor de volgende maand. Vergroot de size op de beste. Dit is het ritme waarin het playbook echt van vorm verandert, en het werkt alleen als de per-trade en wekelijkse ritmes schone rijen aanleveren.

Waarom automatische vastlegging ertoe doet

Als je MFE, MAE en MCE zelf moet typen, doe je het niet. De berekening vraagt dat je elke bar tussen fill en close scant, aan de juiste kant van de positie, en omzet naar geld. Niemand doet dat met de hand om 16:00 op vrijdag. Binnen twee weken zijn de kolommen leeg en is de journal weer gewoon een trade log.

De splitsing is structureel. Het systeem legt execution vast. Jij legt intent en reflectie vast. De Tradeways journal berekent de execution-velden bij close uit 1-seconde OHLCV-bars, zodat MFE, MAE, MCE en realized / MFE al op de rij staan tegen de tijd dat jij regelvolging en de eenregelige notitie invult.

Deze splitsing beschermt ook eerlijkheid. Execution data kan achteraf niet worden aangepast, waardoor wekelijkse en maandelijkse reviews naar dezelfde cijfers kijken als je broker. Intent en reflectie zijn van jou om te schrijven, maar ze staan naast execution data die niet onderhandelt.

Waardoor journals sterven

Drie faalpatronen verklaren bijna elke dode journal.

Te veel velden. Twintig-plus kolommen, waarvan de helft vrije tekst. Ziet er grondig uit op dag een, heeft geen entries meer op dag twintig. Snijd terug naar de set van twaalf tot vijftien velden en weersta toevoegingen.

Geen reviewritme. Rijen stapelen zich op, niemand leest ze. De schrijfkant blijft een maand of twee op momentum draaien en stopt daarna, omdat schrijven zonder lezen niets oplevert. Plan de wekelijkse en maandelijkse reviews als een sessie, niet als een voornemen.

Geen link van review naar volgende week. De maandreview levert interessante charts op, de trader knikt, er verandert niets in het playbook. De loop breekt aan het eind. Een review die niet leidt tot een regelwijziging in het plan voor volgende week, heeft niet plaatsgevonden.

Velden zijn makkelijk. De loop is het moeilijke deel. Houd de rij kort genoeg om hem in te vullen, houd het ritme kort genoeg om hem te lezen, en houd de link expliciet zodat wat je leest verandert wat je tradet.

Gerelateerd

Maximum Favorable Excursion (MFE)

De beste ongerealiseerde winst die een trade bereikte voordat je hem sloot — en wat het verschil met gerealiseerde P&L je vertelt over exits.

4 min leestijd

Maximum Continuation Excursion (MCE)

Wat deed de markt nadat je sloot? MCE meet de beweging die je miste — en laat zien of je exit op tijd was of te vroeg.

6 min leestijd

Marktfases als pre-trade filter

Dezelfde setup wint in het ene regime en verliest in het andere. Classificeer het regime vóór de trade, niet erna.

5 min leestijd