Blog

Maximum Continuation Excursion (MCE)

Was hat der Markt gemacht, nachdem du geschlossen hast? MCE misst die Bewegung, die du verpasst hast, und zeigt, ob dein Exit pünktlich oder zu früh war.

6 Min. LesezeitTradeways#Metriken#Playbook

Maximum Continuation Excursion (MCE) ist die größte günstige Bewegung, die der Markt nach deinem Exit gemacht hat, gemessen in einem Fenster, das mit deiner Haltedauer skaliert. Positives MCE heißt, die Bewegung lief ohne dich weiter. Negatives MCE heißt, der Preis ist kurz nach deinem Exit gedreht, und das ist das sauberste Signal dafür, dass dein Timing gestimmt hat.

Die Lücke, die MFE und MAE offen lassen

Maximum Favorable Excursion und Maximum Adverse Excursion enden beide am Exit-Bar. Sie sagen dir, wie viel Drawdown du ausgesessen hast und wie viel Gewinn drin war, solange die Position offen war. Über den Bar nach deinem Close haben beide nichts zu sagen. Wenn du wissen willst, ob du zu früh ausgestiegen bist, helfen dir MFE und MAE nicht weiter, weil die Daten, die sie betrachten, in dem Moment aufhören, in dem du flach gehst.

Wir haben MCE ins Tradeways-Journal aufgenommen, weil wir eine einzige Zahl brauchten, die über hunderte Trades hinweg die Frage beantwortet: "Bin ich zu früh raus?" MFE und MAE beschreiben den Trade, solange du drin warst. MCE setzt da an, wo sie aufhören, am Exit, und schaut, was danach passiert ist.

Was MCE misst

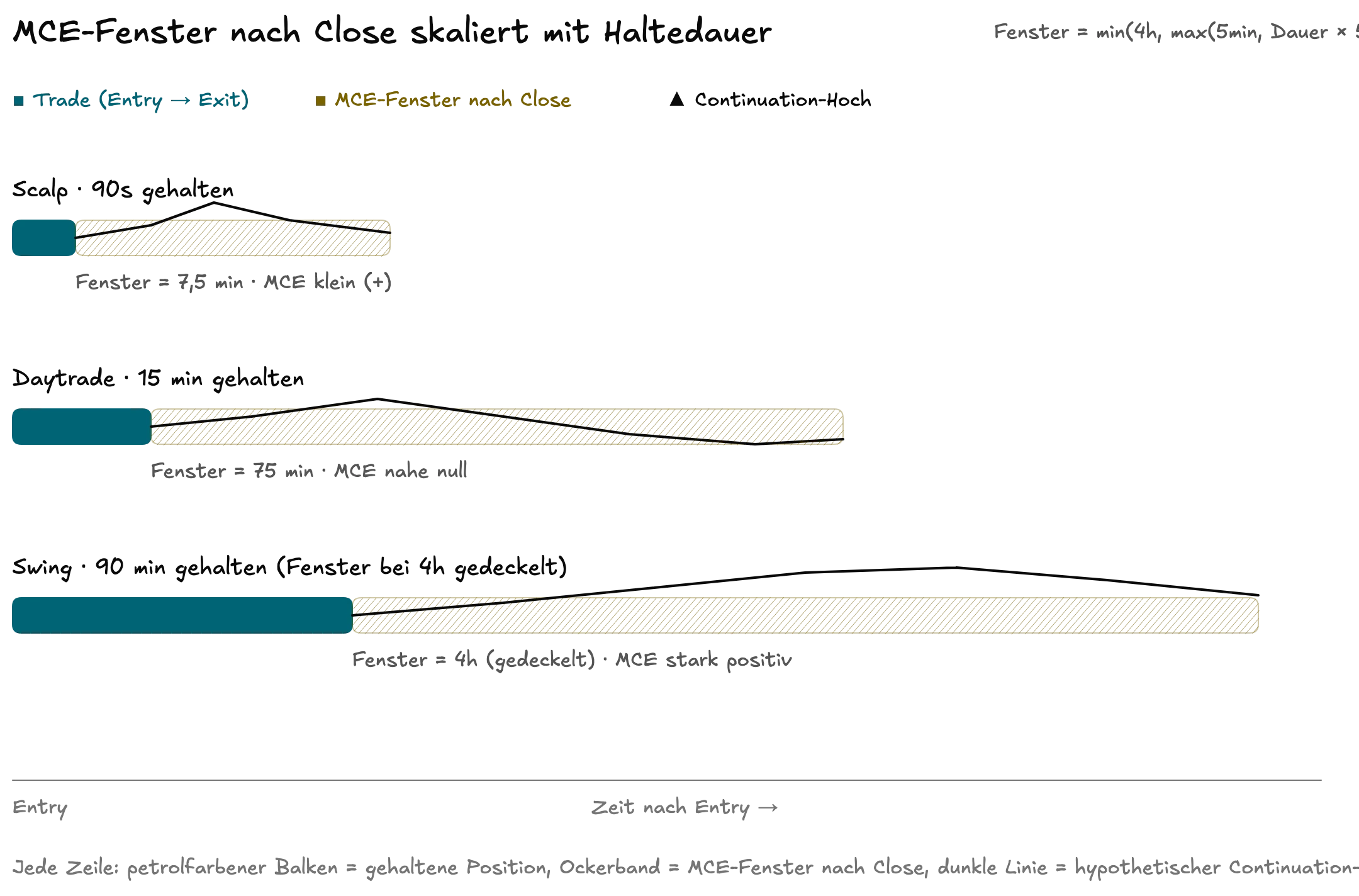

MCE ist der höchste unrealisierte Gewinn, den du gehabt hättest, wenn du drin geblieben wärst, ausgewertet über jeden 1-Sekunden-Bar in einem Post-Close-Beobachtungsfenster. Wir berechnen es aus dem gleichen Databento-Feed (1-Sekunden-OHLCV), den wir auch für MFE und MAE benutzen, damit die drei Zahlen direkt vergleichbar sind.

Daraus ergeben sich drei Signale:

- Großes positives MCE. Die Bewegung lief ohne dich weiter. Dein Exit war zu früh, gemessen an dem, was der Markt geboten hat.

- MCE nahe null. Sauberer Exit. Der Markt hat sich danach weder stark ausgedehnt noch scharf gedreht.

- Negatives MCE. Der Preis ist kurz nach deinem Close gegen dich gelaufen. Dein Exit-Timing hat den Turn erwischt.

MCE ist eine Tradeways-eigene Kennzahl. In der Standardliteratur kommt sie nicht vor. Die Lücke, die sie schließt, ist schmal, aber real: Jede Exit-Diskussion, die du je gelesen hast, behandelt "ich bin zu früh raus" als Gefühl. MCE macht daraus eine Zahl auf jedem geschlossenen Trade.

Warum das Beobachtungsfenster skaliert

Ein 30-Sekunden-Scalp interessiert sich nicht dafür, was in 4 Stunden passiert. Bis dahin hat sich das Regime geändert, die Session ist weitergelaufen, der Order Flow, der den Trade getragen hat, ist weg. Ein 90-Minuten-Swing dagegen kann auch nach 7 Stunden noch relevant sein, weil er auf der gleichen Tagesstruktur lebt.

Die Regel Haltedauer × 5 hält das Fenster proportional zur eigenen Zeitskala des Trades. Das Minimum von 5 Minuten verhindert, dass Rauschen ultrakurze Trades dominiert. Der Deckel bei 4 Stunden verhindert, dass eine mehrtägige Position am Open des nächsten Morgens gemessen wird, was nichts mit deinem Exit zu tun hat. Konkrete Beispiele:

- Ein 90-Sekunden-Scalp bekommt

max(5min, 90s × 5)=max(5min, 7,5min)= ein 7,5-Minuten-Fenster. - Ein 15-Minuten-Daytrade bekommt

max(5min, 75min)= ein 75-Minuten-Fenster. - Ein 30-Minuten-Swing bekommt ein 2,5-Stunden-Fenster.

- Eine 2-Stunden-Position trifft den Deckel bei 4 Stunden.

Positives MCE lesen

Großes positives MCE heißt, du bist zu früh raus. Der Markt ist in deine Richtung weitergelaufen, und du warst nicht mehr dabei. Ein einzelner Trade ist Anekdote, aber ein Muster aus großem positivem MCE auf dem gleichen Setup ist ein struktureller Befund über deine Exit-Regel.

Schau dir das pro Setup an. Wenn MCE auf deinen Scratch-Exits (die, wo du früh rausgegangen bist, weil "irgendwas nicht gestimmt hat") konstant groß und positiv ist, reagiert deine Stop-Verengungs-Logik auf Rauschen, nicht auf echte Drehs. Der Markt hat nicht gedreht, du warst nur nervös, und die Kennzahl beweist es. Wenn MCE auf deinen Target-Exits konstant groß und positiv ist, sitzen deine Targets für dieses Setup zu nah am Einstieg und du solltest sie testweise weiter wegsetzen.

Negatives MCE lesen

Negatives MCE ist der stärkste Beleg dafür, dass eine Exit-Regel wirklich etwas trifft. Ein konstantes Muster aus negativem MCE auf einem bestimmten Setup heißt: Du bist immer wieder rausgegangen, und der Markt ist danach gegen dich gedreht. Das ist kein Rauschen. Das ist deine Exit-Regel, die Turning Points abgreift.

Das ist die seltenste der drei Lesarten, weil die meisten Exits entweder ungefähr pünktlich (MCE nahe null) oder zu früh (positives MCE) sind. Wenn du ein Setup findest, bei dem der Median-MCE über 50+ Trades deutlich negativ ist, hast du etwas Schützenswertes gefunden. Ändere die Regel nicht. Skaliere stattdessen das Setup.

MCE über viele Trades, nicht über einen

Es geht bei MCE nie um die Zahl auf Trade #47. Es geht um den Median über deine letzten 100 Trades, aufgeschlüsselt nach Setup. Ein einzelner Trade sagt nichts aus, weil das Post-Close-Fenster davon dominiert wird, was der Markt zufällig an diesem Nachmittag getan hat. Hundert Trades glätten den Zufall, und die Struktur deiner Exits wird sichtbar.

Eine konkrete Faustregel: Ein Setup mit Median-MCE von +0,3R lässt etwa 30% des Risikos pro Trade an unrealisierter Fortsetzung liegen. Über 100 Trades sind das 30R verpasste Bewegung. Diese Zahl verändert die Diskussion, ob das Setup "gut genug" ist oder ob der Exit überarbeitet werden muss.

Was MCE dir nicht sagen kann

MCE beantwortet eine schmale Frage, und du solltest sie nicht überdehnen. Es kennt deine Re-Entry-Kosten nicht (Slippage, Kommissionen, die Kosten, vor der Fortsetzung ausgestoppt zu werden). Es kennt dein psychologisches Budget nicht, länger im Trade zu sitzen. Es sagt "die Bewegung lief weiter", nicht "du hättest drinbleiben sollen". Drinbleiben heißt meistens, einen weiteren Stop zu akzeptieren, und ein weiterer Stop verändert die Risikoseite auf eine Weise, die MCE nicht sieht.

Behandle es als eine von drei Zahlen, nicht als Urteil. Das vollständige Bild ergibt sich, wenn du MFE, MAE und MCE alle drei zusammen betrachtest: was möglich war, solange du drin warst, wie viel Schmerz du dafür ausgehalten hast und was nach dir noch lief.

MCE in der Praxis

Sobald MCE auf jedem geschlossenen Trade mitläuft, schrumpft das Weekly Review auf eine einzige Schleife.

Es geht nicht darum, sich über verpasste Exits zu ärgern. Es geht darum, "ich glaube, ich gehe früh raus" in eine Zahl zu verwandeln, die sich wöchentlich aktualisiert, und dann die ein, zwei Setups zu finden, bei denen die Zahl groß genug ist, um zuerst angefasst zu werden.

Verwandt

Maximum Favorable Excursion (MFE)

Der höchste unrealisierte Gewinn, den ein Trade vor dem Schließen erreicht hat, und was die Lücke zum realisierten P&L über deine Exits verrät.

4 Min. Lesezeit

MFE, MAE und MCE lesen

Drei Zahlen beschreiben jeden geschlossenen Trade: das Beste, was er wurde, das Schlimmste, was er drohte, und was er nach deinem Ausstieg tat. Zusammen zeigen sie, ob dein Exit strukturell war oder Glück.

2 Min. Lesezeit

Maximum Adverse Excursion (MAE)

Der größte unrealisierte Verlust, den ein Trade überstanden hat, und was deine MAE-Verteilung darüber aussagt, ob deine Stops wirklich arbeiten.

3 Min. Lesezeit