Blog

Marktphasen als Pre-Trade-Filter

Dasselbe Setup gewinnt in einem Regime und verliert im nächsten. Klassifiziere das Regime vor dem Trade, nicht danach.

5 Min. LesezeitTradeways#Playbook#Grundlagen

Dasselbe Setup gewinnt in einem Regime und verliert im nächsten, und die meisten Setup-Post-Mortems sind in Wahrheit Regime-Post-Mortems. Die Lösung ist, das Regime vor dem Trade zu klassifizieren, nicht danach. Ein sauberer Fade gegen das Tageshoch ist auf einem Tape ein Trade mit positiver Erwartung und auf dem nächsten ein struktureller Verlierer, und das Einzige, was sich geändert hat, ist das Regime drumherum.

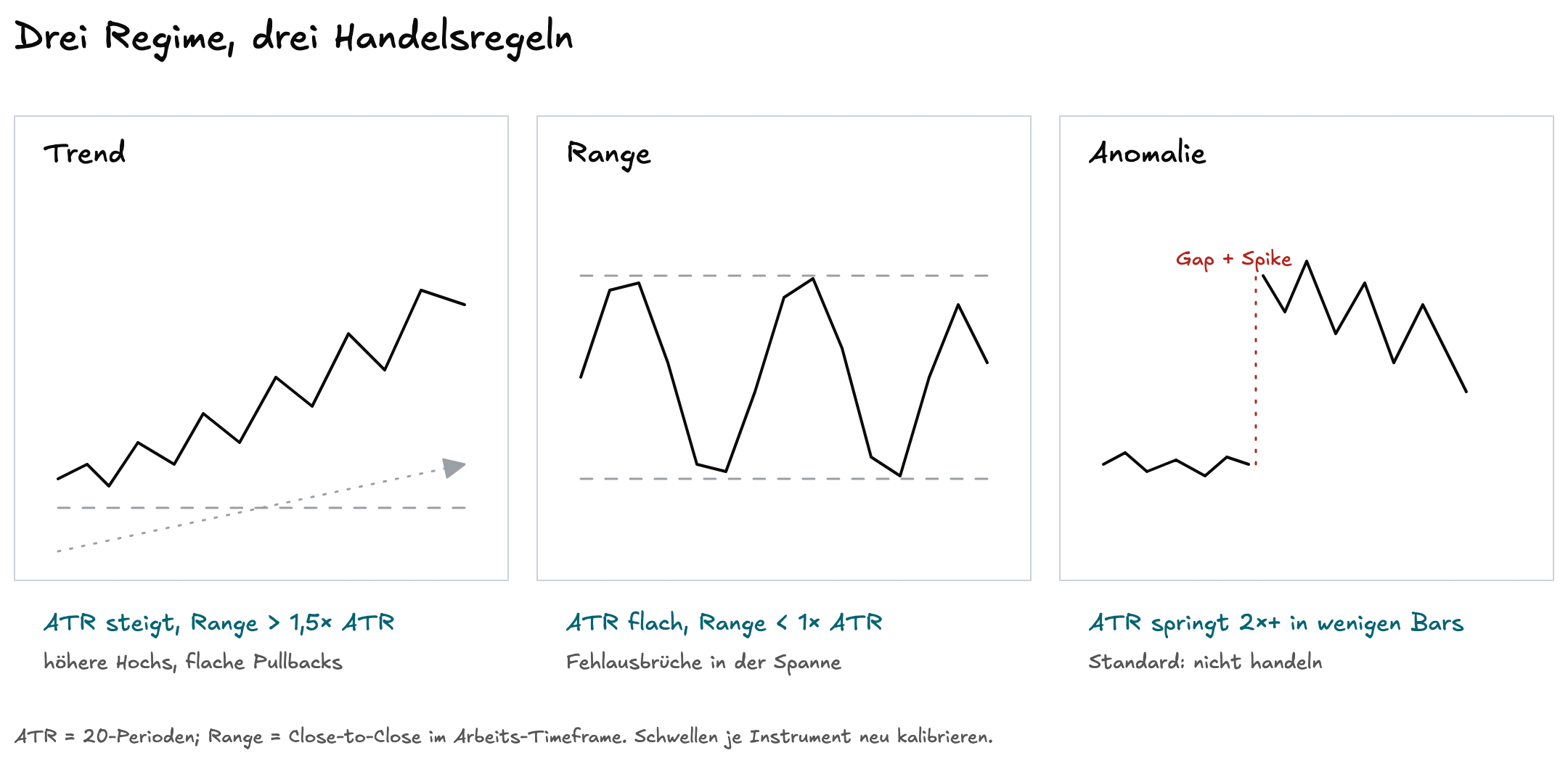

Die drei Regime

Wir arbeiten mit drei. Sie sind operativ definiert, an Zahlen, die du am Chart ablesen kannst, nicht an Bauchgefühl.

Trend. Direktionale Drift dominiert das Rauschen. Operativer Read: Der 20-Perioden-ATR steigt oder ist stabil, während die Close-to-Close-Range im selben Fenster den 1,5-fachen ATR übersteigt. Higher Highs und Higher Lows auf dem Arbeitstimeframe. Pullbacks sind flach und enden über dem letzten Swing-Low. Der VWAP hat eine klare Steigung und der Preis bleibt für den Großteil der Session auf einer Seite davon.

Range. Der Preis oszilliert in einem definierten Band. Der ATR kontrahiert oder läuft flach. Die Close-to-Close-Range liegt unter 1× ATR, der Körper der Bewegung ist also kleiner als der durchschnittliche Bar. Breakouts der letzten N Bars (wir nutzen N = 20 auf dem Arbeitstimeframe) sind gescheitert und in wenigen Bars zurück ins Band gefallen. Der Preis kreuzt den VWAP mehrfach.

Anomaly. Der ATR springt plötzlich, oft um den Faktor 2 oder mehr innerhalb weniger Bars, typischerweise nach einer News-Print, einem Open oder einem Liquiditätsvakuum. Gaps durch vorherige Struktur. Spreads weiten sich. Das Volume Profile zerfällt in dünne Cluster ohne kohärenten Point of Control. Standardumgang: No-Trade-Regime, es sei denn, das Setup ist explizit dafür gebaut und die Size wurde vorher reduziert.

Die Schwellen sind nicht heilig (1,5×, 1×, 20 Perioden). Das sind die Zahlen, die wir am NQ auf dem 5-Minuten-Arbeitstimeframe verwenden. Für dein Instrument und deinen Timeframe musst du sie neu kalibrieren. Wichtig ist, dass die Regel mechanisch ist und an jedem Tag dieselbe Zahl produziert, damit die Klassifizierung im Journal nachvollziehbar bleibt.

Warum Setups das Regime interessiert

Setups haben keine Erwartung im Abstrakten. Sie haben Erwartung in einem Regime.

Ein Mean-Reversion-Fade gegen das Tageshoch ist im Range ein Trade mit positiver Erwartung, im Trend ein Münzwurf und in der Anomaly ein Stop-Out. Gleicher Entry-Trigger, gleicher Stop, drei verschiedene Ergebnisse, weil die Auction, die den Fade fängt, nur existiert, wenn der ATR kontrahiert und der Breakout über dem letzten Hoch gescheitert ist. Im Trend feuert derselbe Trigger, während der Breakout echt ist und das nächste Higher High der Open des nächsten Bars ist. In der Anomaly wird der Stop durchschlagen, bevor die Order überhaupt gefüllt ist.

Für Continuation gilt das Umgekehrte. Ein Breakout-Pullback-Long ist das Brot des Trend-Regimes und das langsame Leck des Range-Regimes. Im Range triggert er genau dort, wo die gescheiterten Breakouts liegen, und du kassierst kleinen Verlust nach kleinem Verlust an genau der Stelle, an der du statistisch am häufigsten falsch liegst. Das Setup ist nicht kaputt. Du hast es im falschen Regime genommen.

Wenn ein profitables System aufhört zu funktionieren, hat sich meistens das Regime bewegt, bevor das System sich bewegt hat. Der Trader schließt, dass der Edge tot ist. Das Journal, wenn es auf jedem Trade das Regime taggt, zeigt, dass der Edge im nativen Regime intakt ist und die jüngsten Verluste alle im fremden liegen.

Wie Regime mit MCE zusammenhängt

Continuation-Bewegungen häufen sich in Trend-Regimen. Das ist keine stilistische Aussage, das ist die Definition des Regimes. Wenn du Trades mit MCE taggst, konzentriert sich der High-MCE-Tail auf Trend-Tagen, weil die Post-Exit-Drift dort einen Ort hat, an den sie laufen kann.

Die praktische Konsequenz: Wenn du MCE nach Setup zerlegst und ein Setup mit fettem positiven Tail findest, ist der nächste Schnitt nach Regime. Sind die High-MCE-Trades fast alle Trend-Regime-Trades, dann scheitert die Exit-Regel nicht zufällig. Der Exit ist auf das durchschnittliche Regime ausgelegt und wird vom Trend-Regime gekappt, also genau in dem Regime, in dem die Continuation des Setups lebt. Die Korrektur ist regime-bewusst: längere Haltedauer, ein Trailing Stop oder schlicht ein anderer Exit an Trend-Tagen. Die Kennzahl hat es dir schon gesagt. Erst das Regime macht das Signal lesbar.

Ein praktischer Pre-Trade-Check

Drei Fragen, in dieser Reihenfolge, vor jedem Entry.

Das ist eine 30-Sekunden-Disziplin, keine Analyseaufgabe. Die Regime-Zahl ist berechnet, sobald der Bar geschlossen ist. Die Erwartung-pro-Regime-Zahl steht schon im Journal. Schritt (c) ist der einzige, der Charakter verlangt.

Was du in Echtzeit nicht klassifizieren kannst

Regime-Übergänge sind im Rückblick offensichtlich und in Echtzeit glitschig. Die ATR-Regel hinkt strukturell nach. Du siehst das Trend-Regime zwei Bars nach der Bewegung bestätigt, die es etabliert hat. Diese Lücke ist nicht zu vermeiden. Vermeidbar ist nur, so zu tun, als gäbe es sie nicht.

Wir bauen einen Übergangs-Flag in dieselbe Berechnung ein. Wenn der 20-Perioden-ATR die Richtung wechselt (steigt nach Fallen oder fällt nach Steigen) und die Close-to-Close-Range zwischen 1× und 1,5× ATR liegt, feuert keine Regel sauber. Das ist die Zwischenzone. Die Regel lautet dann nicht "Regime wählen und committen", sondern "Size halbieren, Frequenz halbieren, warten". Eine halbierte Position überlebt einen falschen Regime-Call. Eine volle Position bei unklarer Klassifizierung ist der Trade, der die Wochengewinne genau dort vernichtet, wo du am wenigsten Information hattest.

Die ehrliche Version: Das Regime ist immer eine Wahrscheinlichkeit, kein Fakt. Der Sinn der operativen Regel ist nicht, daraus einen Fakt zu machen, sondern die Wahrscheinlichkeit jeden Tag zur selben Zahl zu machen, damit die Trades vom Dienstag mit denen vom letzten Dienstag vergleichbar sind und das Journal seine Arbeit machen kann. Der Trader, der jeden Tag mit derselben Regel klassifiziert und sich an den unklaren Tagen heraushält, schlägt den Trader, der an drei Tagen im Jahr das Tape brillant liest.

Verwandt

MFE, MAE und MCE lesen

Drei Zahlen beschreiben jeden geschlossenen Trade: das Beste, was er wurde, das Schlimmste, was er drohte, und was er nach deinem Ausstieg tat. Zusammen zeigen sie, ob dein Exit strukturell war oder Glück.

2 Min. Lesezeit

Maximum Favorable Excursion (MFE)

Der höchste unrealisierte Gewinn, den ein Trade vor dem Schließen erreicht hat, und was die Lücke zum realisierten P&L über deine Exits verrät.

4 Min. Lesezeit

Maximum Continuation Excursion (MCE)

Was hat der Markt gemacht, nachdem du geschlossen hast? MCE misst die Bewegung, die du verpasst hast, und zeigt, ob dein Exit pünktlich oder zu früh war.

6 Min. Lesezeit